In 1651 the philosopher Thomas Hobbes warned that a nation’s sovereign needs a reliable stream of taxation revenue. Without properly funded law and order there would be “perpetuall warre [sic] of every man against his neighbour”. Updating Hobbes, the risk of our lives turning out to be economically difficult would be lessened if the Australian Treasury could lift its game in forecasting revenue.

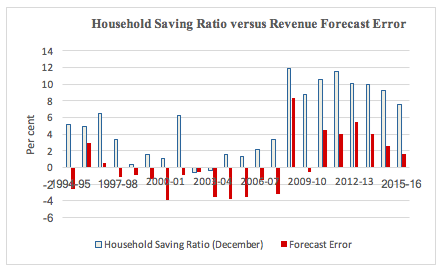

During the Costello era (1996-2007), Australian budgets underestimated tax receipts for the upcoming fiscal year on eleven out of twelve occasions. More of a worry was the Swan-Hockey era (2007-2015), which saw tax receipts being overestimated for eight fiscal years in a row. For an illustration of this, see Chart 1 below.

Fortunately, help is at hand from information on the household saving ratio, which is household net saving as a percentage of household net disposable income. The relevant data can be found in the December-quarter national accounts, released a couple of months before each budget. In the December 2016 National Accounts, for example, the ratio came in at 5.2 per cent. Combined with existing budget forecasts, this information can be deployed to mitigate the chronic patterns of error in Treasury’s revenue forecasts.

Saving behaviour is intelligent and forward-looking, not mechanical or fixed. Households tend to save when they believe their current income is temporarily high, and dissave when they believe their current income is temporarily low.

By signalling the hopes and fears of households, the saving ratio becomes a useful input to budget forecasts.

The saving ratio impounds forward-looking information not only about the outlook for private-sector revenues from exports but important demographic changes, notably, the impending retirements of the three-quarters of baby boomers still at work. Along with weak commodity prices, these adverse demographics exert downward pressure on revenues.

Chart 1 below shows the household saving ratio is variable rather than fixed. It also reveals a positive correlation between the ratio and subsequent errors (forecasts minus outcomes) in budget forecasts of growth in nominal tax revenues.

Chart 1

Source: Lance A. Fisher and Geoffrey Kingston, “Improved Forecasts of Tax Revenue via the Permanent Income Hypothesis”, The Australian Economic Review, vol.50, no.1, pp.21-31.

The correlation between each December-quarter value of the household saving ratio and the revenue forecast error in the subsequent fiscal year is 0.84, confirming that data on the saving ratio can improve the accuracy of revenue forecasts.

It’s possible to estimate the actual numbers needed to combine the raw Treasury forecasts – which do contain much valuable information, despite their patterns of error – with the extra information available in the saving ratio. Without spelling out the technical details of the statistical number crunching, here’s what it implies for the current fiscal year.

The 2016 Budget papers predicted that Commonwealth tax receipts would grow by 5 per cent in nominal terms over the current financial year. The household saving ratio in the December quarter of 2015 was 7.5 per cent. In conjunction with estimates of the weights needed to produce a combination forecast, these two inputs imply the Treasury forecast for tax receipts growth over 2016-17 needed to be adjusted downwards a little:

2016-17 revenue forecast adjusted via the December 2015 saving ratio

= 4.0 + 0.83 × Predicted Tax Receipts Growth – 0.63 × Household Savings Ratio

= 4.0 + 0.83 x 5 − 0.63 x 7.5

= 3.4 per cent.

If this calculation turns out to be correct, the inaugural Morrison budget (2016) will mark the ninth successive occasion on which tax revenue growth has been over-estimated.

By the same token, the predicted extent of over-estimation will have been only 1.6 percentage points, compared with an average of 3.6 percentage points for the Swan-Hockey era. The reason is the December-quarter household saving ratio in 2015 was down to 7.5 per cent compared to its peak of 12.6 per cent in 2008. So there appeared to have been a lot less income pessimism on the part of households in the December quarter of 2015 than during the global financial crisis of 2008.

Fiscal year 2016-17 is shaping up as a year of two halves. The National Accounts for September 2016 reported a drop in real output growth. In its Mid-year Economic and Financial Outlook published in December 2016, Treasury trimmed back its May 2016 forecast of tax revenue growth over 2016-17.

By February 2017, however, it was clear that last year’s rises in commodity prices were continuing. Moreover, the National Accounts for the December quarter of 2016 reported a sizeable drop in the saving ratio, to 5.2 per cent. This fall augers well for revenue growth over calendar 2017.

Incorporating the latest information, then, last May’s tax revenue forecast for 2016-17 may well turn out to be Treasury’s most accurate budget forecast since 2009-10.

Wouldn’t the correlation between the forecast errors and the *change* in the HSR (as opposed to the *level* of the HSR) be more informative about the relationship?

Hi Matt

Thanks for your comment. However, we think the level of HSR–as distinct from its rate of change–is the right explanatory variable in a predictive setup like ours. Put another way, differencing HSR would constitute “over-differencing”. Our 2005 article in the Journal of Money, Credit and Banking sets out the relevant theory.

Have you ever considered that the level of private household debt to GDP may have an impact on HSR?

Hi Wayne

Thanks for your comment. As a matter of accounting, a runup in the ratio of household debt to GDP will tend to go hand in hand with a lower saving ratio, and we’ve seen this in the recent data. However, most rises in household debt are associated with higher equity in houses, often via capital gains. HSR doesn’t capture increases in household wealth via capital gains, as explained in the concluding section of our 2017 paper in the Australian Economic Review.

Thanks Geoff and Lance excellent point, will read that paper. Has anyone measured the HSR using the GNP instead of GDP?

Hi Wayne

Thanks for your follow-up comment. Actually, HSR is already based on an income measure of Australian activity (i.e. output by Australian citizens) rather than a product measure (i.e. output within Australia’s borders).

Thanks Geoff and Lance.

Pingback: Open Budget Survey 2017 Part 2: What Can Australia Do to Improve Our Budget Process? - Austaxpolicy: The Tax and Transfer Policy Blog