On budget night, we heard that there is going to be an adjustment to the third income tax threshold, so that the 37 per cent income tax rate will apply from $87,000 rather than $80,000. We were told that this change was made to correct the tax system for bracket creep.

However, bracket creep has the greatest impact on the low-middle income range, and when combined with the announced compensation package that favours high-income earners, results in an income tax system that is less progressive than existed 12 months ago. The expiration of the Temporary Budget Repair Levy only reinforces this trend.

Bracket creep occurs because we have a progressive income tax system , and the thresholds of this system are defined in nominal terms. This means that if someone earned an amount that increased only with inflation (meaning that they earn the same amount each year in real terms), they would slowly move into higher income tax brackets.

Bracket creep also affects people who don’t move between tax brackets, as it results in a lower proportion of their income being taxed at lower marginal tax rates. For instance, as inflation increases the nominal value of your paycheck, a smaller proportion of this paycheck falls under the tax-free threshold, and a larger proportion falls under your highest marginal tax rate.

The easiest way to show the total incidence of bracket creep is a simple simulation exercise. This exercise calculates the amount of income tax paid at a given level of income in 2015-16, and then applies 2 per cent bracket creep (which is equivalent to reducing the nominal values of the tax thresholds by 2 per cent) and recalculates the amount of tax payable.

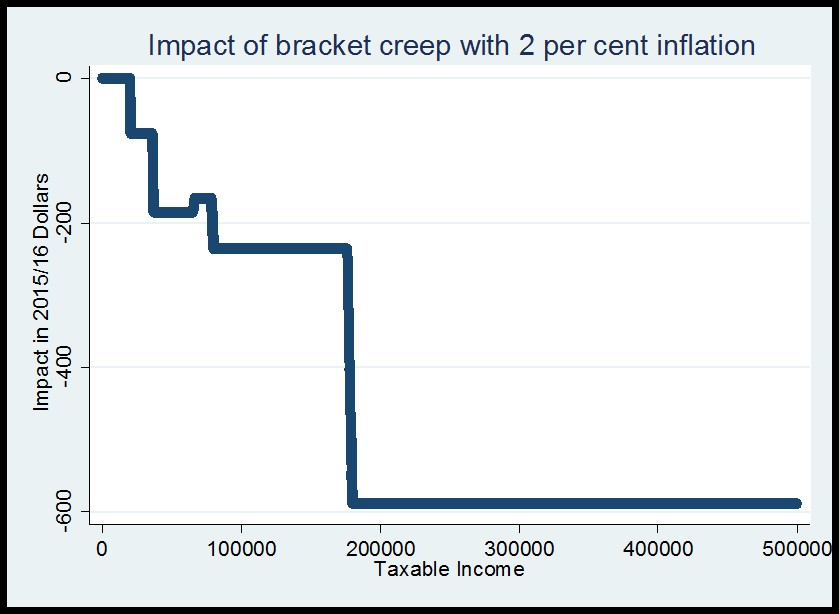

The chart below shows the dollar impact of bracket creep. Specifically, it shows the difference in tax paid after bracket creep (the calculation includes the tax thresholds, deficit repair levy and low income tax offset, but not other elements of the tax/transfer system).

This chart can also be interpreted as the amount that would be gained by each individual if the tax thresholds were indexed to inflation.

Source: Author’s own calculations.

This shows that the impact of bracket creep resembles a set of stairs, with each step occurring at a tax threshold in the income tax system. (The small step up around $80,000 follows from after the phase out of the Low Income Tax Offset where the marginal tax rate drops slightly.)

We can also see that there is an absolute limit (about $600) of how much bracket creep can affect a high-income earner. This occurs because they are already in the top income tax bracket. As the total impact of bracket creep is that less income falls under the lower tax rates, this effect will be the same whether the person is earning $200,000 or $500,000.

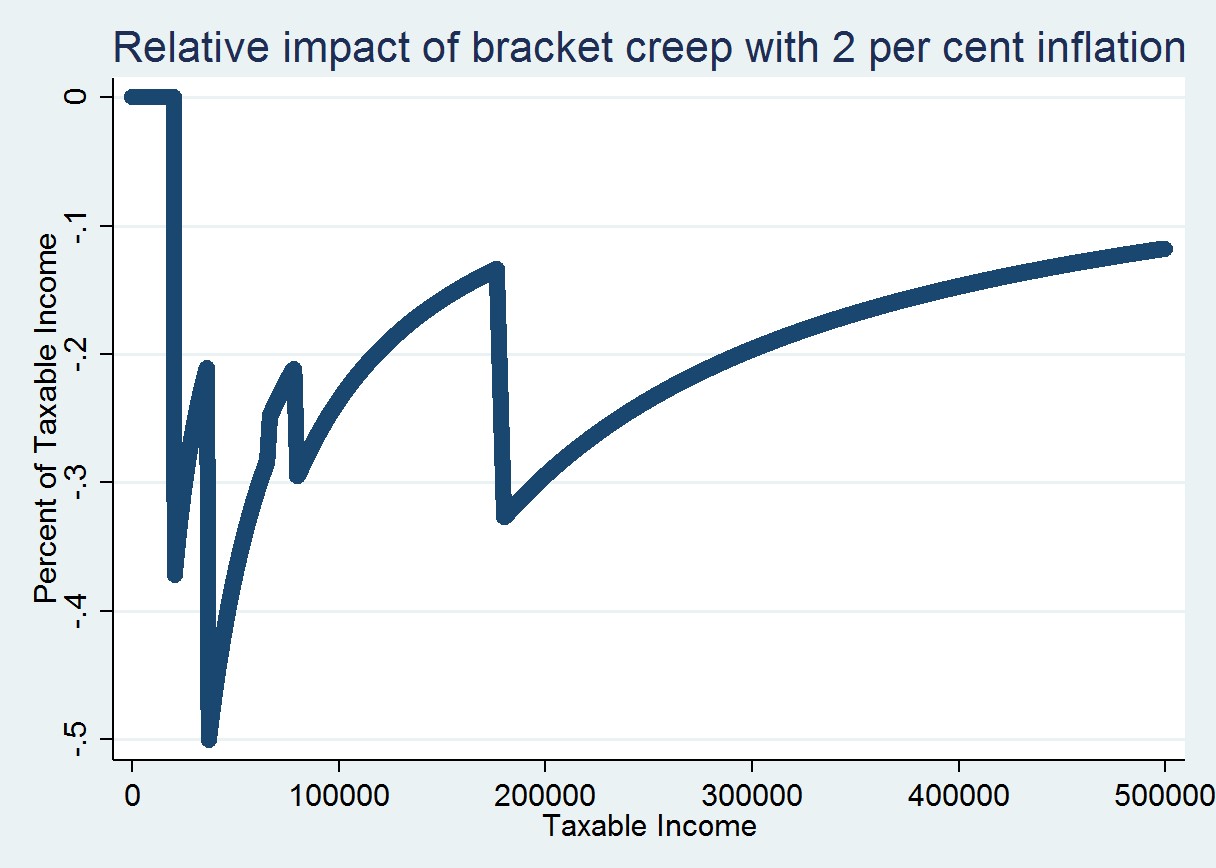

The previous chart showed the absolute impact of bracket creep across the income distribution. However, when looking at distributional impact it is normal to look at the impact as a percentage of current income. This is because a percentage of current income is a better measure of ability to pay tax. This measure is shown in the following chart.

Source: Author’s own calculations.

The relation between taxable income and the percentage of total income reveals that the impact of bracket creep is neither progressive or regressive, but follows a ‘v‘ shape, with the heaviest impact on low to middle income earners and the smallest effects on very low and high income earners.

This suggests that if we were concerned about the tax burden being driven by bracket creep, it would make sense to focus tax relief on low-middle income earners (people earning $30,000 – $60,000). For a person earning $37,000, bracket creep has the largest impact, equivalent to 0.5 per cent of taxable income.

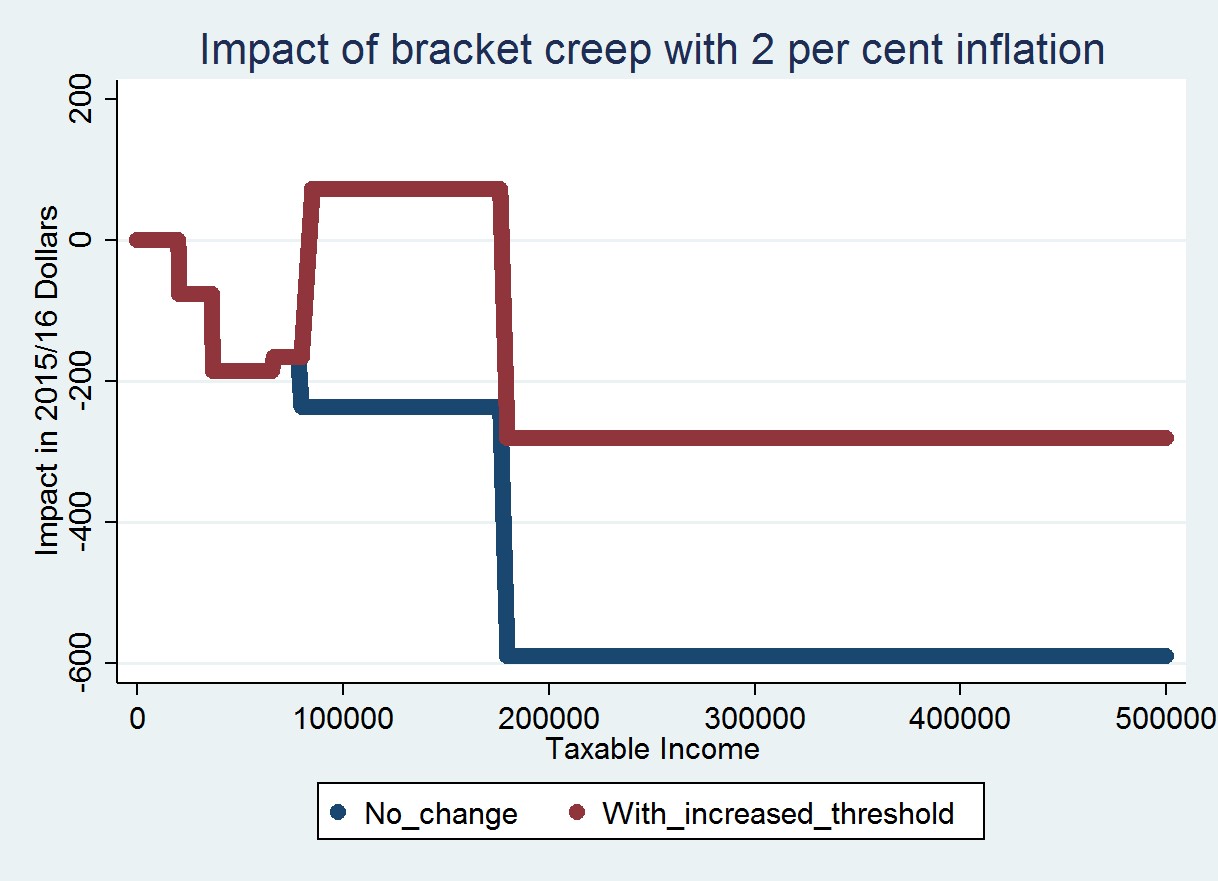

Instead, the measure in the budget is provided to all people earning over $80,000. The following chart shows the combined impact of 2 per cent bracket creep and the increase in the tax threshold.

This chart shows that people earning $87,000 – $180,000 are more than fully compensated for bracket creep by this increase in the $80,000 threshold. In the following chart, the blue line shows the impact of bracket creep, while the red line shows the combined impact of bracket creep and the compensation package.

Source: Author’s own calculations.

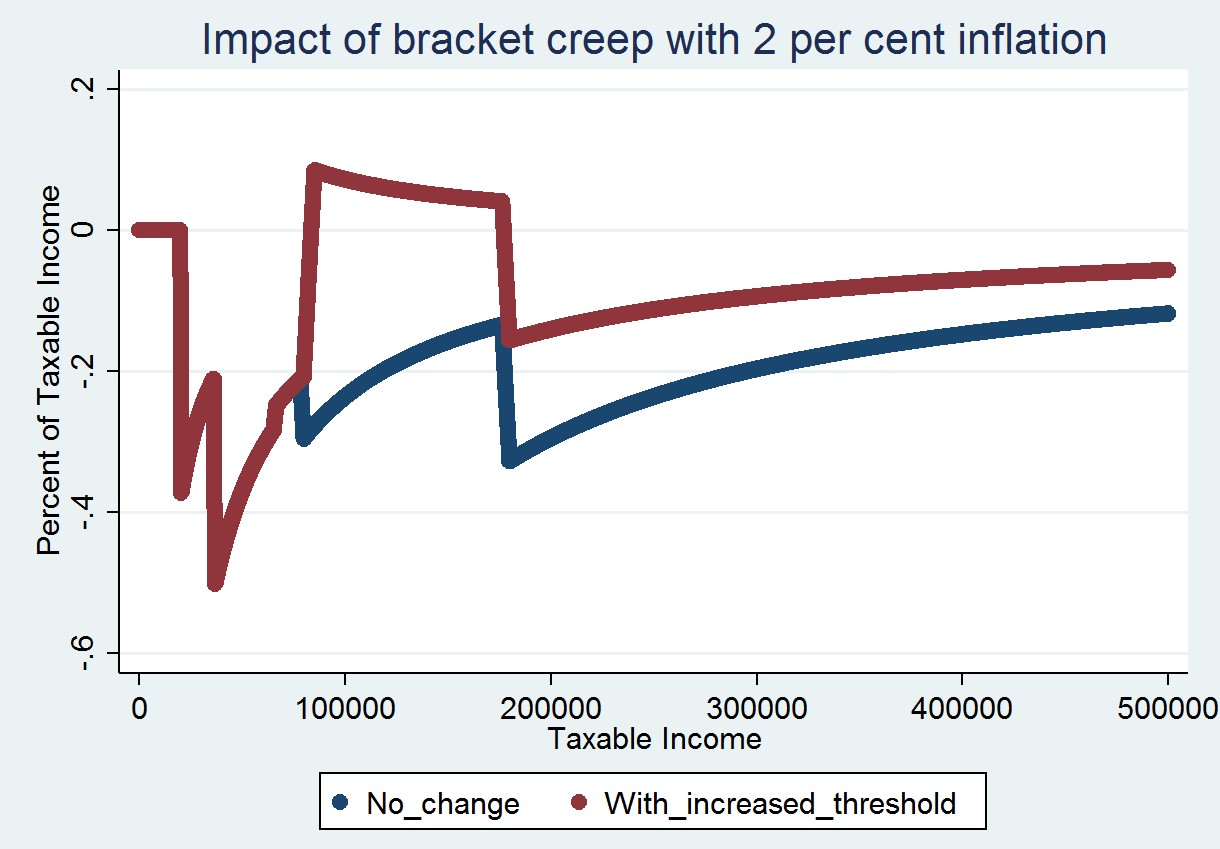

The targeting of this compensation package only looks worse when examining incidence as a percentage of total income. We see that low-middle income earners that are hit hardest receive no compensation, while higher income earners are left either better off, or only slightly worse at the end of the period.

Source: Author’s own calculations.

What about the Budget Repair Levy?

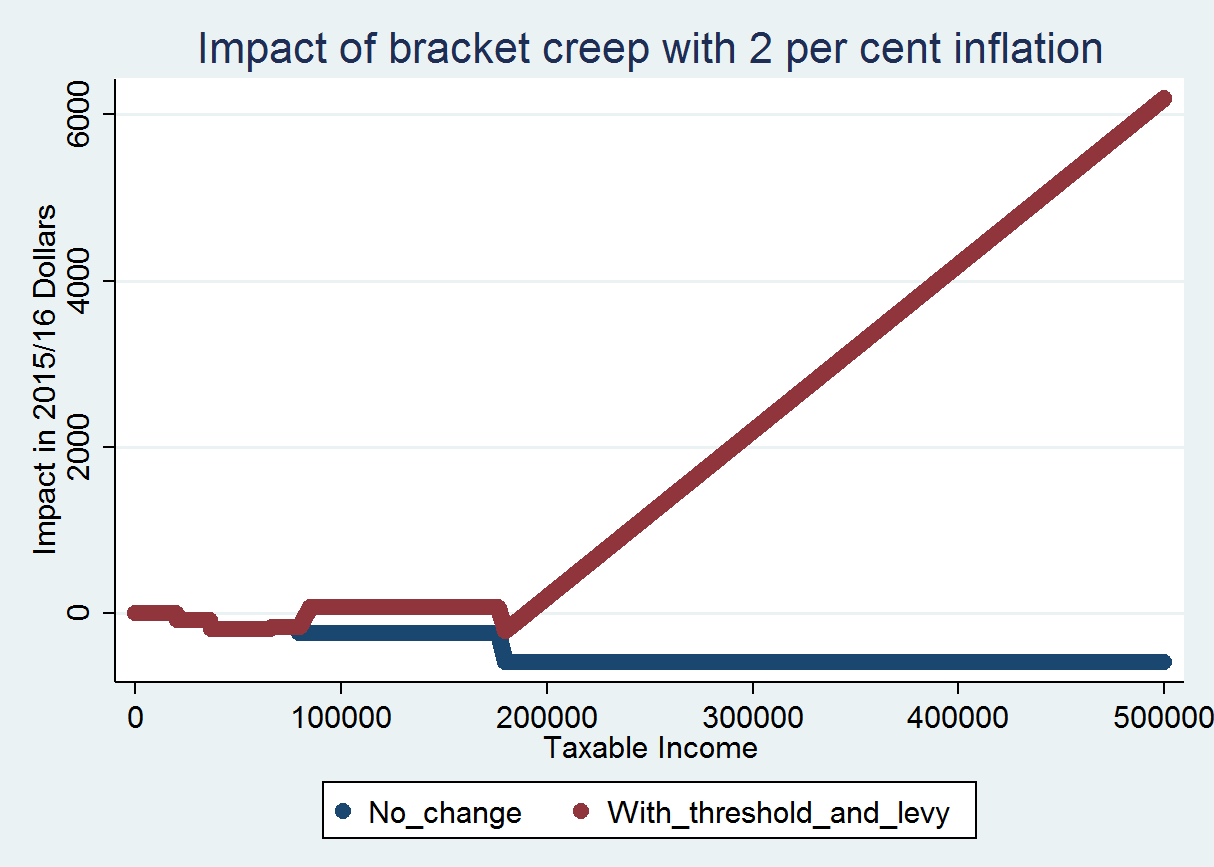

We can also examine the effect of the ending of the Temporary Budget Repair Levy on progressivity of the tax rate scale. The next chart shows the incidence of bracket creep compared with both the announced adjustment to the $80,000 tax threshold and the removal of the 2% Temporary Budget Repair Levy, which applies to income above $180,000.

Source: Author’s own calculations.

Some caution needs to be exercised here. There are only a small number of people earning $300,000 compared to lower incomes. Nevertheless, it is clear that the expiry of the Budget Repair Levy reinforces the bracket creep adjustment in making the tax system less progressive.

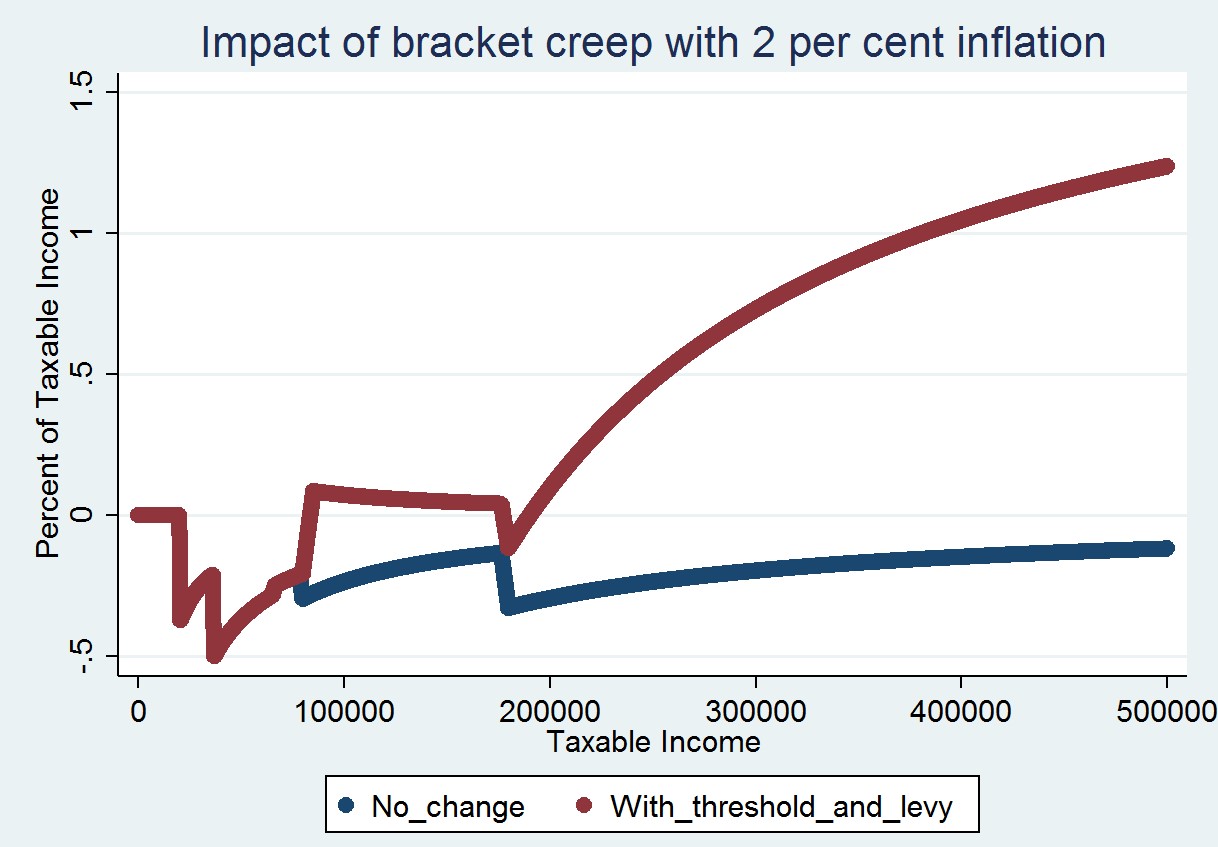

A similar picture emerges when looking at this combination of polices as a percentage of income.

Source: Author’s own calculations.

It is possible that the announcements in the budget are driven by other considerations. For instance, it is possible that pushing people into higher tax brackets may reduce the incentive to work for this group and reduce the amount of labour supplied in the Australian economy. However, there is little evidence that this effect would be large, and it is not clear why people earning $80,000 to $87,000 are special in this regard. The Treasurer also stated that budgets in previous years provided support for low-income earners (for example, the carbon tax compensation package was targeted at lower income earners), and so this budget could be targeted at a different income group.

Nevertheless, this simple exercise shows that the announcements in the budget have made the Australian income tax less progressive than it was one year ago, and that if the changes were designed to respond to bracket creep, they are poorly designed for this task. This reduction in progressivity should be announced and debated explicitly, rather than being obfuscated through so-called adjustments for bracket creep.

Recent Comments